Time under water: the metric your backtest ignores.

Systematic books model max drawdown but almost never model recovery time. Time-under-water reveals what allocators actually experience, and it belongs in your monthly reporting.

- Time-under-water measures the longest stretch an equity curve spent below a previous peak.

- Allocators stress-test recovery time before they stress-test drawdown depth.

- A clean recovery curve from a deep drawdown is the strongest single signal an emerging manager can show.

What is time-under-water, and why does it matter?

Systematic books usually model max drawdown. They calculate it, target it, set a stop on it. The metric they almost never model is how long it takes to climb back out.

Time-under-water (TUW) measures the longest stretch the equity curve spent below a previous peak. A book with a 5% max drawdown that recovers in three weeks behaves nothing like a book with the same 5% drawdown that takes ten months to recover. The headline DD number masks what an allocator actually experiences.

Allocators stress-test recovery time before they stress-test depth. The reason is committee-level: a 12-month TUW means a manager spends a full annual review cycle explaining flat returns. Most committee chairs have seen exactly how that conversation ends.

What does the MAR ratio tell you?

The MAR ratio (CAGR divided by max drawdown) is the rough first cut. It rewards strategies whose long-run compounding offsets drawdown depth. Strategies whose CAGR is small relative to depth score poorly. A MAR above 1 is the floor for serious institutional conversations. Below that, the baseline return is doing too much work.

What drives recovery time at the book level?

Two things drive recovery time at the book level.

First, the structural choice of whether you de-risk during drawdown or hold size through it. De-risking shortens depth and extends recovery, because the smaller book has less compounding base when conditions normalise. Holding size accepts deeper drawdown in exchange for faster recovery once the regime turns. The choice has documented implications either way, and allocators want to see it written down before drawdown hits.

Second, strategy correlation under stress. The matrix gives you the time-averaged number. Recovery time surfaces the worst single stretch. A book of nominally uncorrelated strategies that all hit drawdown together has a longer recovery profile than the average correlation suggests (classic regime-overlap problem).

A clean recovery curve from a deep drawdown is the strongest single signal you can show.

Why does recovery profile matter for emerging managers?

For an emerging manager, recovery profile is where you have real influence in the allocator conversation. A clean recovery curve from a deep drawdown is the strongest single signal you can show. That story beats "we never drew down more than 4%" because every committee chair has seen managers who never drew down 4% until they drew down 30%.

How should you measure drawdowns in practice?

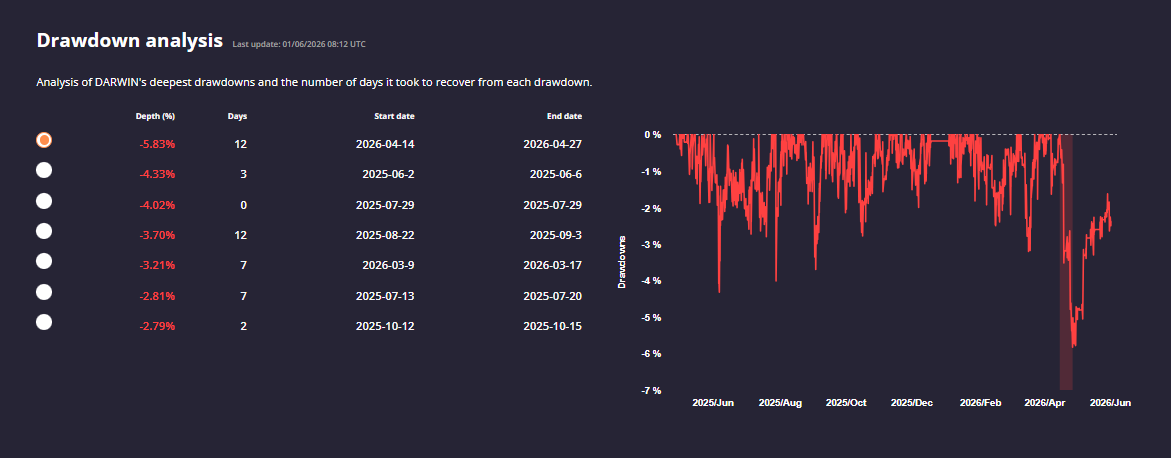

Below is a look at my Drawdown Analysis of XAQP. You can see, we're measuring both depth and time when looking at the drawdowns. It's important to know whether you're skewed more towards deeper drawdowns, with a higher recovery factor, or shallower drawdowns with a lower recovery factor.

Build TUW into monthly reporting. Track it alongside max DD, Sharpe, Sortino, and Calmar for a complete picture of what allocators actually evaluate. Position sizing drives how deep the drawdown goes in the first place, which is why the maths of ruin should inform every sizing decision.

Disclosure. Kieran Duff is an employee of Darwinex (Tradeslide Technologies Ltd). This letter is personal commentary, not Darwinex investment advice.

Capital at Risk. Past performance is not indicative of future results. Nothing in this letter constitutes investment advice, a solicitation, or an offer to buy or sell any financial instrument.

Performance figures are before fees (gross), denominated in USD, and reflect the live track record of XAQP since inception on 28 April 2025, as managed under Darwinex (Tradeslide Technologies Ltd). Returns are gross of costs; actual investor returns will be lower after fees.

Get the next letter in your inbox.

By subscribing you agree to our Privacy Policy.